Ideally, accounting professionals should receive payment for every service they bill, on time, every time. Obviously, we don't live in a perfect world, and businesses often have to consider what they can do about their end-of-year finances when debt is on their books. With the help of this year-end accounting checklist, you can process your receivables and, eventually, collect those outstanding accounts, perhaps even those you've almost forgotten about.

For accounting professionals, the year-end closing process involves taking an in-depth look at a company's financial transactions and ledgers over the past fiscal year, with the ultimate goal of creating a finalized financial record. So what does all of that entail, exactly?

This is by no means an exhaustive list; the steps required can also vary depending on the nature of the business going through the year-end accounting process.

A full accounting of the company's finances is required to accurately perform year-end closing activities for a company. One of the most significant issues that often comes up when an accounting professional is digging through the books is discovering that certain items are missing, unaccounted for, or not accounted for properly. A missing invoice or receipt can delay the process significantly, requiring the professional to track down who might be responsible for the missing transaction or detail and rectify the issue as soon as possible.

Likewise, simple human error can cause significant headaches for end-of-year accounting. If, for instance, a massive spreadsheet has an error or typo, it can create an inaccurate view of a company's finances, throwing off projections for the next year and forcing the professional to try and find the discrepancy. Even if a professional tries to automate the process, a misclick or a typo in their formula can result in equally inaccurate data.

Of course, when data is missing, chasing it down can become a hassle. Some employees or relevant parties supposed to have the data may not have it readily on hand, which could lead to delays while they attempt to track it down. In worst-case scenarios, the relevant parties may not provide the correct information or may not have access to the data anymore.

While some of these issues are not always foreseeable or preventable, they are nevertheless important considerations for any accounting professional looking to perform end-of-year accounting for any client. The more prepared a professional can be for the worst, the better off the entire process will go.

Thankfully, there are many ways for accounting professionals to maximize the success rate of their year-end closing activities. The following checklist can help prevent the process from feeling overwhelming and ensure you have covered all the essential bases nearly any company will need for their year-end closing.

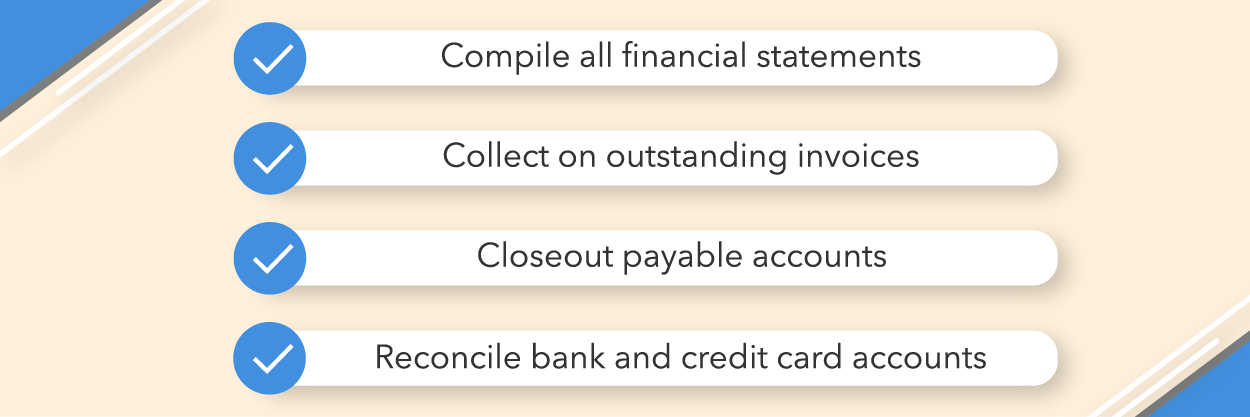

A good starting point is to collect all of the financial statements of the company undergoing the year-end closing process. These can include any of the following:

Ideally, all of these items would already be in a digital format. If not, scanning these documents to turn them into digital ones is recommended. Scanning these vital documents will help serve as a backup system in case they are lost or destroyed. In the long run, digital copies will be significantly easier to deal with, as modern accounting technology can access them and expedite processing their contents.

Obviously, this is challenging, as you won't always have control over whether your clients pay your bills on time (or at all). If you have invoices yet to be paid, your best bet will be to categorize them based on how likely you think a payment will be before the end of the fiscal year. Generally speaking, the younger the unpaid invoice is, the more likely you'll be able to coerce a payment out of the client in question.

Next, send out a mass email reminding these clients of their outstanding balances. Ideally, this should come from the professional who handled the client's account (or is still handling it). The professional may even ask for a lower amount than what is owed. While this may sound like a crazy idea, getting paid any amount for the invoice is better than collecting absolutely nothing from it.

Learn more about how to collect unpaid invoices in our ebook, Year-End Accounting Guide: Closing on Strong Financial Footing.

Any outstanding balances or invoices the business owes should be noted and resolved to maintain a healthy cash flow going into the new year. Make sure you speak to the necessary parties at the company and have them make these payments as soon as possible.

You may also need to follow up with the relevant parties to ensure there are no issues on their end. Sometimes a payment may have been rejected or lost in the mail. Creating a proper follow-up process with the business can help minimize outstanding invoices.

Bank account reconciliation and credit card reconciliation are essential elements of a business's year-end accounting checklist. It is absolutely critical that bank records match accounting records to ensure that reconciliation happens seamlessly.

Thoroughly investigate these records and see if any discrepancies are discovered. It may be necessary to adjust one of your records to make the balances equal.

An accounting firm undergoing the year-end closing process should have easy access to its income statement. This document is essential in determining whether you had a year that exceeded expectations (with record profits and goals met) or fell short of expectations (with lost money and unforeseen expenses). An income statement is also helpful in determining how solid the firm's bottom line will be going into the new year, as it can project patterns throughout the fiscal year and help the business make informed decisions going forward.

Naturally, the end of the year is an excellent time to begin creating goals for the new year. Aside from carrying over any plans that have already been put in place, try making a list of goals the entire company can work towards. We recommend following the S.M.A.R.T. system (Specific, Measurable, Achievable, Relevant, and Time-Sensitive).

When these parameters are defined according to your goal, you will be able to ensure that your objectives are achievable within a certain period of time. By defining specific goals and timelines, clearing up less-defined ideas, and identifying milestones that have been missed, this approach can help you laser-focus your ideas and ensure your plans can be actualized in the coming year.

It's also a solid idea to review your firm's practices and see where any improvements can be made. A more streamlined firm can produce faster results and better serve its clients in the long run.

The first step might be to create a roadmap that explains your firm's policies regarding payments and how much the engagement will cost. If your firm is the right fit for the client, you need to determine how they intend to pay for your services. You should include all of this information in your fee agreement.

You may also consider getting ahead of your accounts receivable and billing methods by following up with them in advance. Check your bills' payment status about a week after they are sent by setting a reminder on your calendar. Then reach out to these clients to ensure the bill is top of mind.

Modern accounting technology can work wonders within your organization and when assisting clients. One of the easiest and most effective ways to upgrade your current technology stack is by implementing an online payment solution. These versatile software solutions enable you to expand your payment options to accommodate a variety of billing situations and best practices. For example, CPACharge allows you to send your clients a Quick Bill, instantly generating a payment request with a convenient link to pay your bill by credit card or eCheck. These Quick Bills can also be tracked to see if the client has viewed the bill and whether their payment is on the way.

The end-of-year accounting process can feel daunting for any business, including your own. However, these techniques can turn a write-off into substantial revenue.

Learn more about optimizing your year-end accounting by reading our ebook, Year-End Accounting Guide: Closing on Strong Financial Footing.